AI Is Slowing Down

When growth becomes a requirement.

Part I — The Industry Already Spent the Money

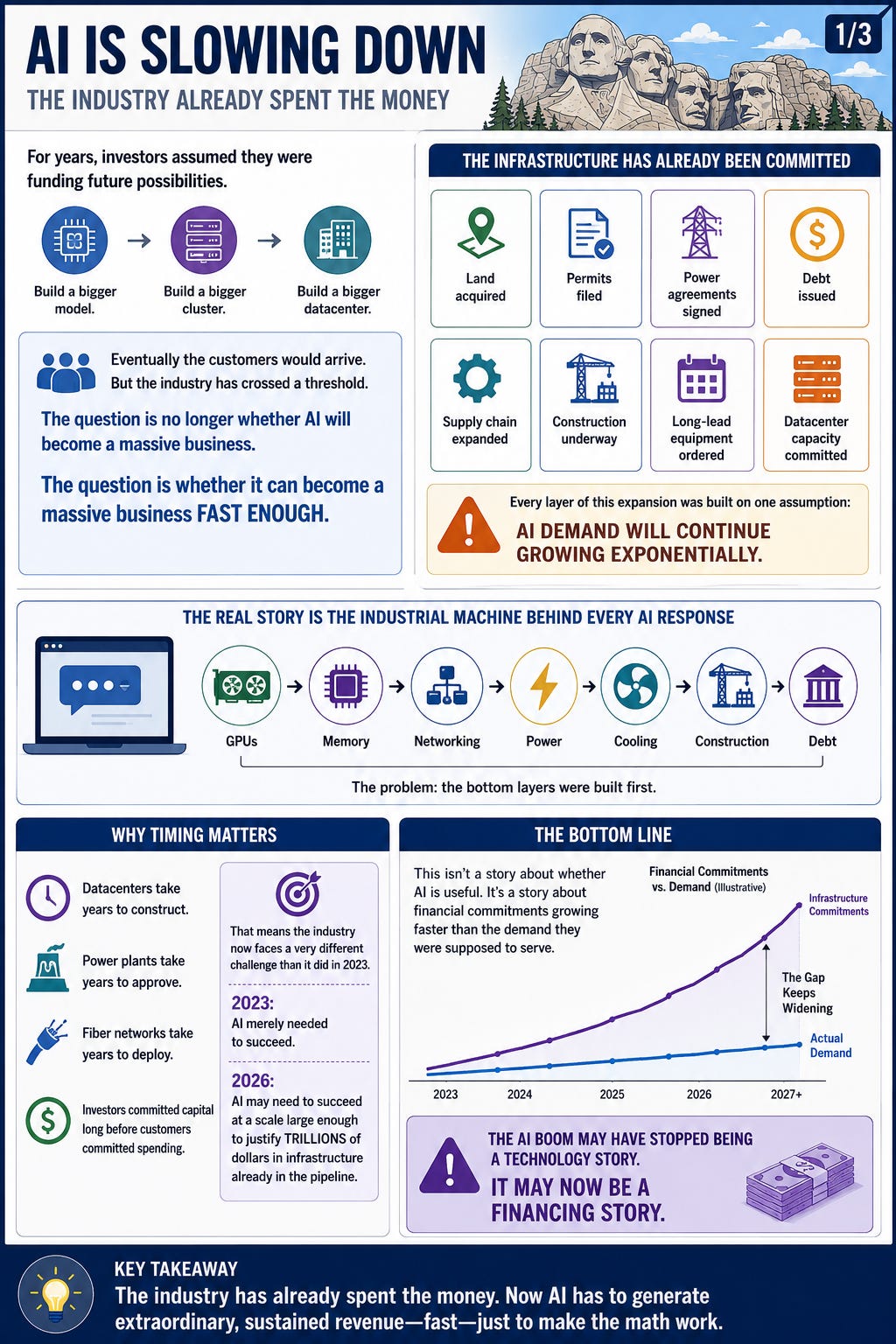

For most of the AI boom, investors assumed they were funding future possibilities.

Build a bigger model.

Build a bigger cluster.

Build a bigger datacenter.

Eventually the customers would arrive.

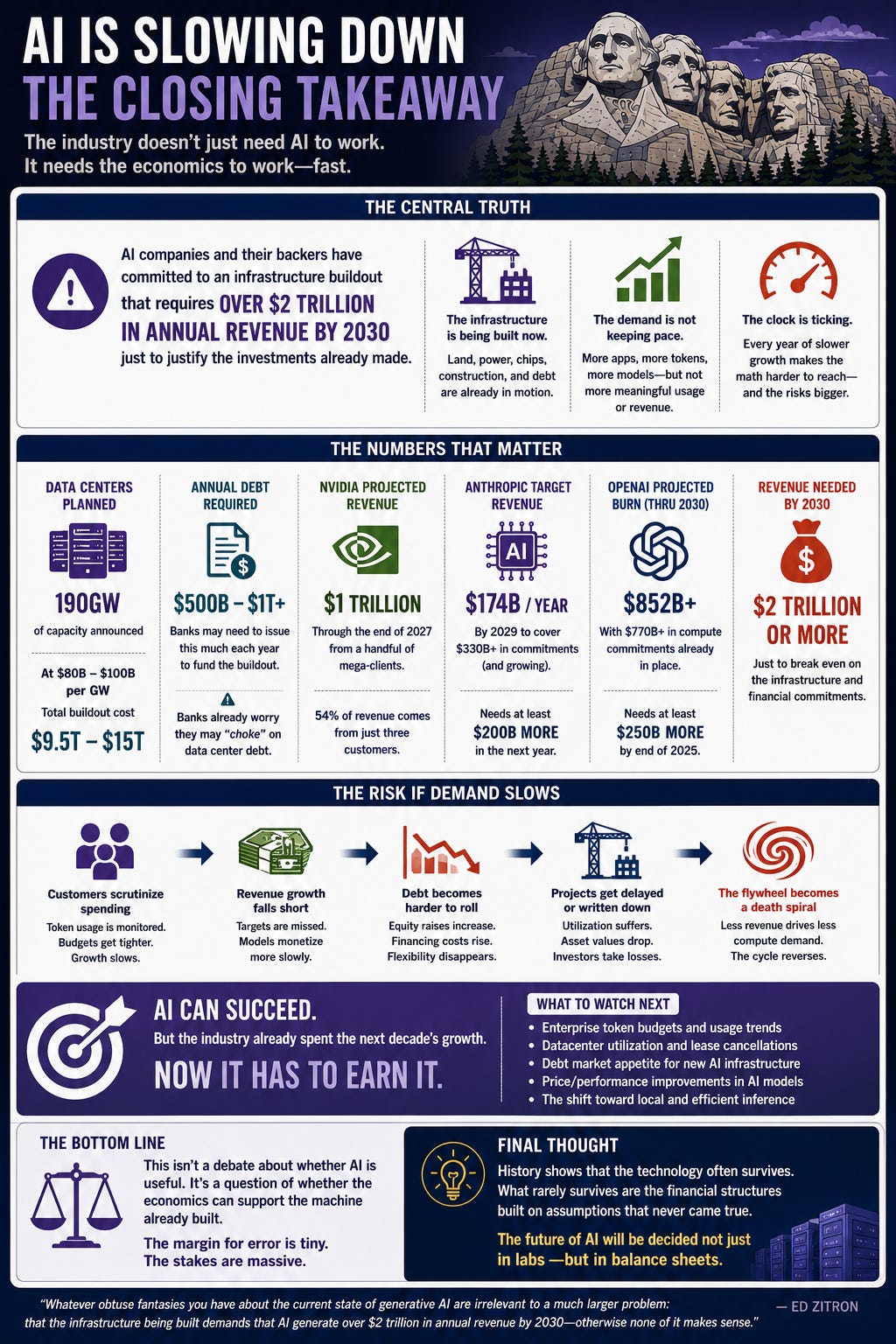

But Ed Zitron's latest analysis argues that the industry has quietly crossed a threshold. The question is no longer whether AI will become a massive business. The question is whether it can become a massive business fast enough.

The reason is simple.

The infrastructure has already been ordered.

The land has been acquired.

The permits have been filed.

The power agreements have been signed.

The debt has been issued.

The supply chain has expanded.

And every layer of that expansion was built on one assumption:

AI demand will continue growing exponentially.

For years the narrative focused on the models themselves. GPT-4. Claude. Gemini. OpenAI. Anthropic.

But the real story may be buried underneath them.

Every AI response sits on top of an enormous industrial machine:

AI Services

GPUs

Memory

Networking

Power

Cooling

Construction

Debt

The problem is that the bottom layers were built first.

Datacenters take years to construct.

Power plants take years to approve.

Fiber networks take years to deploy.

Investors committed capital long before customers committed spending.

And that means the industry now faces a very different challenge than it did in 2023.

Back then, AI merely needed to succeed.

Today, AI may need to succeed at a scale large enough to justify trillions of dollars of infrastructure that is already moving through the pipeline.

That is the core insight behind Zitron's article.

Not that AI is useless.

Not that AI has no customers.

But that the financial commitments being made appear to be growing faster than the demand they were supposed to serve.

In other words:

The AI boom may have stopped being a technology story.

It may now be a financing story.

Part II — The Demand Problem

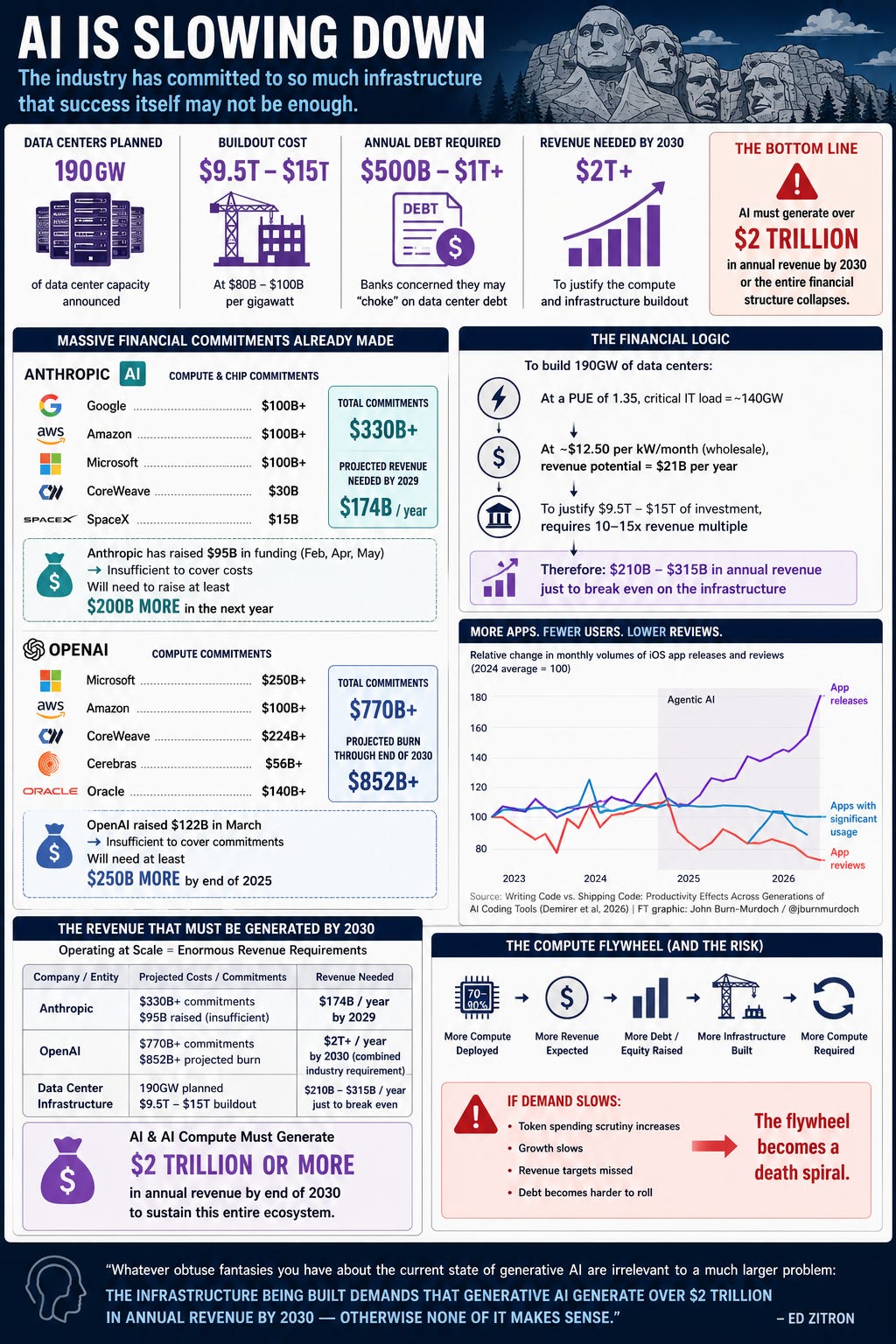

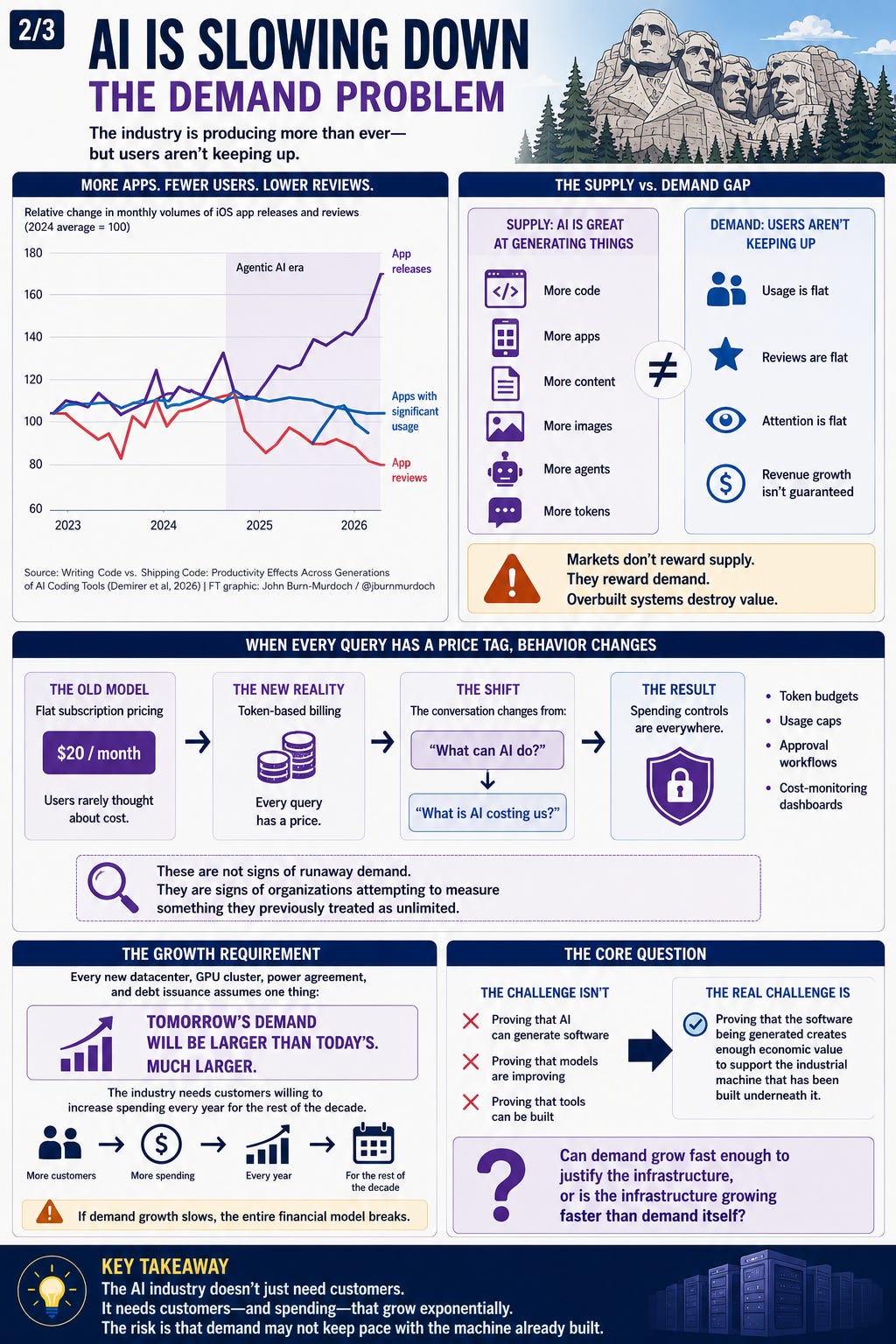

The most uncomfortable chart in Zitron's article isn't about OpenAI, Anthropic, or NVIDIA.

It's a chart showing app releases and app usage.

Moving in opposite directions.

According to the data, AI-assisted software development is producing more applications than ever before. New apps are flooding into app stores at an accelerating pace.

But user engagement isn't following.

Reviews are flat.

Usage is flat.

Attention is flat.

The machine is producing more output, but not necessarily more value.

That distinction matters.

For years, AI advocates have focused on supply.

How much faster can software be written?

How many more apps can be produced?

How many more features can be shipped?

But markets don't reward supply.

They reward demand.

A factory that doubles production without doubling customers doesn't become twice as valuable.

It becomes overbuilt.

And that may be the risk emerging across the AI economy.

The industry has become remarkably good at generating things:

More code

More apps

More content

More images

More agents

More tokens

Yet the question investors ultimately care about is much simpler:

Who is paying for all of it?

This becomes especially important as companies begin moving away from flat subscription pricing and toward token-based billing.

When AI was bundled into a $20 monthly subscription, users rarely thought about cost.

When every query has a price tag attached to it, behavior changes.

Finance departments start asking questions.

Managers start imposing limits.

Engineers start looking at dashboards.

Suddenly the conversation shifts from:

"What can AI do?"

to

"What is AI costing us?"

That shift may explain why we're starting to see spending controls appear across the industry.

Token budgets.

Usage caps.

Approval workflows.

Cost-monitoring dashboards.

These are not signs of runaway demand.

They're signs of organizations attempting to measure something they previously treated as unlimited.

And once measurement begins, assumptions start colliding with reality.

The AI industry doesn't merely need customers.

It needs customers willing to increase spending every year for the rest of the decade.

Because every new datacenter, GPU cluster, power agreement, and debt issuance assumes that tomorrow's demand will be larger than today's.

Much larger.

The challenge isn't proving that AI can generate software.

The challenge is proving that the software being generated creates enough economic value to support the industrial machine that has been built underneath it.

That's the question hanging over the entire AI economy:

Can demand grow fast enough to justify the infrastructure, or is the infrastructure growing faster than demand itself?

Part III — When Growth Becomes a Requirement

Every investment bubble eventually encounters the same question:

What happens when growth slows?

Not collapses.

Not reverses.

Simply slows.

For most businesses, slower growth is manageable.

A retailer can open fewer stores.

A manufacturer can reduce production.

A software company can cut costs and focus on profitability.

But AI may be different because the ecosystem has become dependent on growth itself.

OpenAI needs more compute.

The cloud providers need OpenAI.

The datacenter builders need the cloud providers.

The power companies need the datacenter builders.

The equipment vendors need everyone.

Each layer is relying on the next layer continuing to expand.

The result resembles a giant industrial flywheel.

More AI Demand

More Revenue

More Capital Raised

More Datacenters Built

More Compute Available

More AI Demand

As long as demand grows, the flywheel accelerates.

But if demand grows slower than expected, the entire machine begins to feel friction.

That doesn't necessarily mean AI disappears.

The internet survived the dot-com crash.

Fiber networks survived the telecom bubble.

Cloud computing survived years of skepticism.

The technology often survives.

The financial structure built around the technology may not.

That's the distinction investors sometimes forget.

History is full of examples where society eventually adopted a technology while the first generation of companies, financiers, and infrastructure investors lost fortunes getting there.

Railroads.

Telecom.

Solar.

Fiber optics.

The technology was real.

The timing was wrong.

The financing was wrong.

The expectations were wrong.

That possibility hangs over AI today.

Because the numbers now being discussed are no longer measured in billions.

They are measured in trillions.

Trillions of dollars of projected infrastructure.

Trillions of dollars of projected compute demand.

Trillions of dollars of expected future revenue.

And that means the margin for error becomes very small.

A modest slowdown in customer spending can ripple through every layer of the stack.

A delay in enterprise adoption can affect datacenter utilization.

A push toward efficiency can reduce demand for compute.

A shift toward local models can weaken the economics of centralized infrastructure.

Ironically, some of the industry's greatest technical successes could become financial problems.

If models become dramatically cheaper to run, fewer datacenters may be needed.

If local AI becomes common, fewer tokens may be sold.

If efficiency improves faster than demand grows, the revenue assumptions supporting today's buildout begin to weaken.

That is why Zitron's article feels different from earlier critiques.

It isn't arguing that AI doesn't work.

It is asking whether the economic machine built around AI has become larger than the demand currently supporting it.

The real risk may not be technological failure.

The real risk may be that the industry spent the next decade's growth before the next decade arrived.